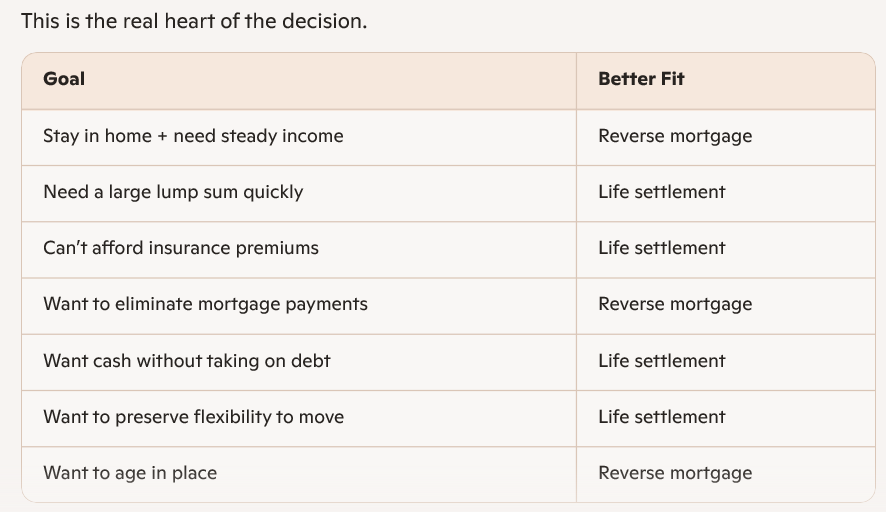

Why People Look at Reverse Mortgages and Life Settlements

People consider reverse mortgages and life settlements for the same core reason: they need cash in retirement, and these tools unlock money tied up in long‑held assets—either home equity or life insurance. Both options convert illiquid value into usable funds, but they do so in very different ways.

What is a reverse mortgage?

A reverse mortgage allows homeowners age 62 or older to borrow against their home equity without making monthly mortgage payments. The most common type is the Home Equity Conversion Mortgage (HECM), which is insured by the Federal Housing Administration (FHA).

Instead of making payments to a lender, the loan balance grows over time and is typically repaid when the borrower sells the home, moves out permanently, or passes away. As long as borrowers meet ongoing requirements, they retain ownership of the home and can continue living there.

For people who want to stay where they are, that can be the main appeal. The money can help with medical expenses, accessibility upgrades, or everyday living costs. But it’s not a neutral choice. Fees add up, interest compounds, and the equity left behind may be much smaller than expected.

It also isn’t fast. Reverse mortgages involve counseling and a longer approval process, which protects borrowers but requires patience.

While a reverse mortgage can provide long-term cash flow and flexibility, it isn’t free money. Upfront costs and ongoing interest cause the loan balance to grow over time, reducing the equity remaining in the home.

Borrowers must also continue paying property taxes, homeowners insurance, and maintenance costs. And because the loan is repaid from the home’s value, heirs may inherit less equity.

What is a life settlement?

A life settlement involves selling an existing life insurance policy to a third-party investor for a cash payment. The buyer takes over premium payments and receives the death benefit when the insured person passes away.

The payout is typically more than the policy’s cash surrender value, but less than the full death benefit. Life settlements are generally considered by older policyholders who no longer need or want their coverage.

This option often comes up when a policy no longer serves its original purpose. Children are grown. Debts are paid. Estate plans have changed. In those cases, the policy can function more like an asset than a legacy tool.

Pricing depends heavily on age and health, which can feel uncomfortable to think about. Longevity-focused asset managers evaluate expected lifespan and future costs when valuing policies, which is why overviews of lifespan-based financial solutions can help explain how those numbers are actually calculated.

To qualify for a life settlement, you typically need to:

- 1. Be over age 65

- 2. Have a whole life, universal life or other permanent policy with a death benefit of at least $100,000

- 3. Have held the policy for at least two years (which varies by state)

- 4. Have changes in your health status since you purchased the policy

Neither option is simple financially. Reverse mortgages involve upfront fees and ongoing interest. Life settlements may include broker commissions and can have tax consequences depending on how much was paid into the policy over time.

How Reverse Mortgage Funds Are Typically Used vs. Life Settlement Proceeds

Reverse mortgages and life settlements both convert illiquid assets into cash, but retirees tend to use the money very differently because one is a loan tied to the home and the other is a sale of an insurance policy.

Key Differences in How the Money Gets Used

| Feature / Use Case | Reverse Mortgage Funds | Life Settlement Proceeds |

| Nature of funds | Loan advances (must be repaid) | Cash from selling a policy (no repayment) |

| Typical payout form | Monthly income, lump sum, or line of credit | One‑time lump sum |

| Most common uses | Ongoing living expenses, paying off mortgage, healthcare, emergency line of credit | Paying for care, eliminating debt, replacing lost income, stopping premium payments |

| Asset at risk | Home equity (and potentially the home if taxes/insurance lapse) | None of your property is at risk; policy is sold |

| Tax treatment | Generally not taxable | May be taxable depending on basis and gain |

| Long‑term impact | Reduces home equity over time | Eliminates death benefit for heirs |

The Practical Pattern

- Reverse mortgage funds are usually used like a slow‑release income supplement—monthly cash flow, paying off the existing mortgage, or covering ongoing expenses.

- Life settlement funds are usually used like a financial reset button—a lump sum to eliminate premiums, pay for care, or restructure finances without taking on debt.

Do you need real estate services? RE/MAX Achievers Can Help You!

Contact Us!

Contact our offices in Pottstown or Collegeville!

Collegeville: 610-489-5900

Pottstown: 610-326-1200

OR through our social media pages!

Facebook and Instagram at “REMAXAchieversAgentsinPA”

Instagram:

Facebook:

https://www.facebook.com/SouthEasternPARealEstateSalesAgents